Digital nomads need more than Wi-Fi. Learn how a monthly reset with bookkeeping, budgeting and goal checks helps sustain life abroad.

The dream of digital nomadism is usually painted with vibrant colors. It’s the laptop on a beach, the bustling café in Berlin, or the quiet mountain cabin in northern Thailand. We talk a lot about the freedom, the gear and the best travel insurance. But there’s a quieter, less glamorous side to this lifestyle that determines whether you stay on the road for six months or six years. It’s not about your Wi-Fi speed or your packing list of things not to forget. It’s about the rhythm you keep when the world around you is constantly changing.

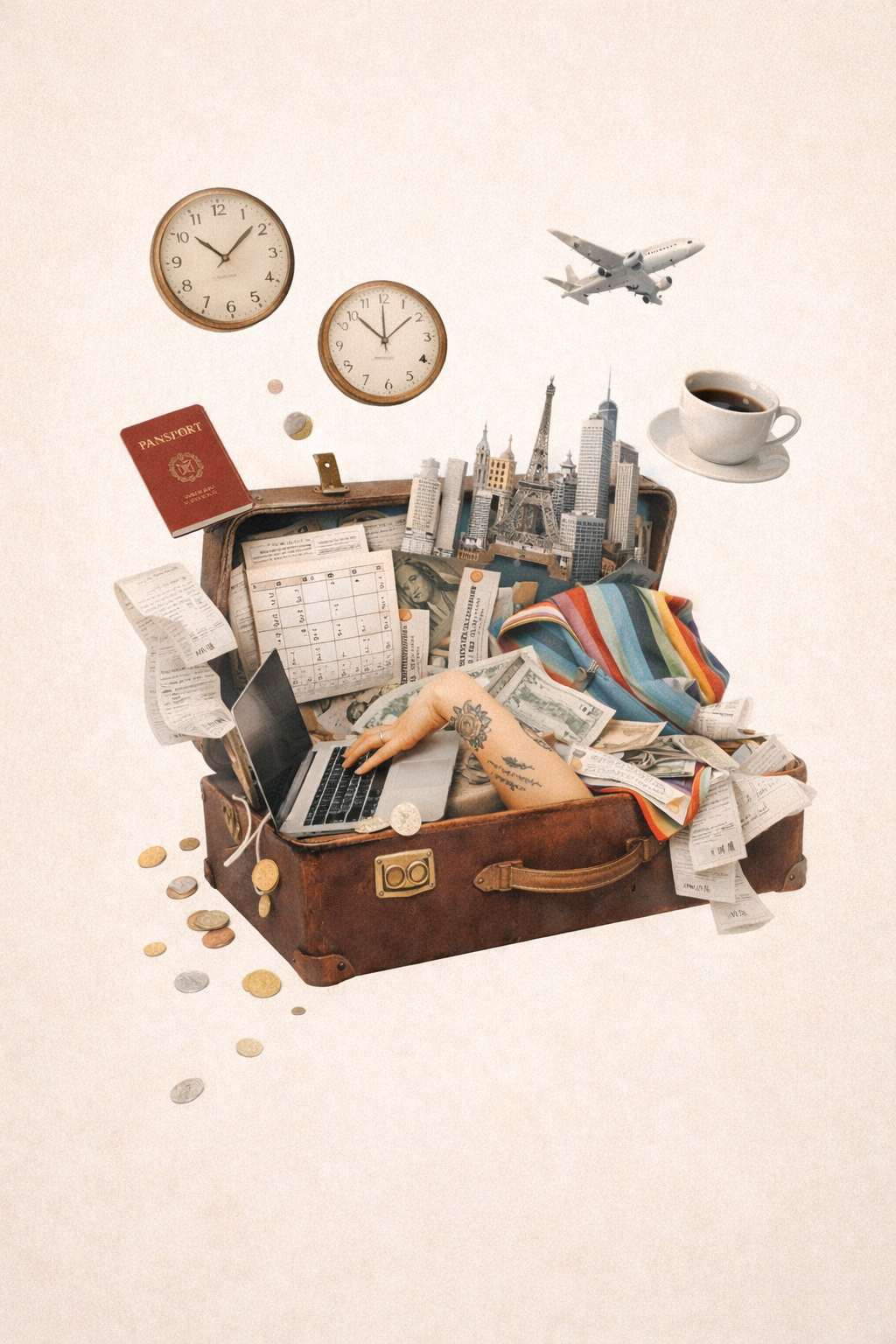

Then there’s the logistics of moving abroad. When you live out of a suitcase, everything is fluid. Your timezone shifts. Your currency changes. Even the taste of the coffee is different. While that variety is exactly why we do this, it can also be our undoing. Without a solid anchor, the lack of structure eventually leads to burnout or financial stress. But there’s one specific routine that sits at the intersection of your professional success and your personal peace of mind: the monthly reset.

Why the Monthly Reset Matters for Digital Nomads

Most people think of routines as daily things. We have our morning coffee or our evening stretching. For a nomad, daily routines are easily broken by a flight or a bad connection. A monthly routine, however, is a bird’s-eye view. It is your chance to stop being a passenger in your own life and start being the pilot again.

The monthly reset is a dedicated block of time where you look at your finances, your projects and your health. It’s the moment you acknowledge that you spent too much on ride-sharing apps in Mexico City or that you haven’t spoken to your best friend back home in weeks. It’s about catching the small leaks before they sink the ship.

Financial Clarity on the Road

The most critical part of this routine is facing the numbers. It’s very easy to lose track of spending when you’re constantly converting prices in your head. One day you feel like a king, and the next, everything seems expensive and you’re wondering where your savings went.

Establishing a consistent habit for your finances is non-negotiable. This involves more than just checking your bank balance. It means categorizing your expenses and ensuring your taxes are being handled. Taking the time to follow a guide to monthly bookkeeping ensures that your business remains healthy while you explore. When you know exactly what’s coming in and what’s going out, the freedom of nomadism actually feels real because it’s backed by data.

“A monthly routine is your chance to stop being a passenger in your own life and start being the pilot again.”

The Mental Health Checkpoint

Nomadism is lonely. We don’t talk about that enough. You meet a lot of people — but you have very few deep roots. Part of your monthly routine should be an audit of your social and mental well-being.

Are you feeling burned out? Have you stayed in one place long enough to learn the name of the person at the grocery store? If the answer is no, your monthly reset is the time to pivot. Maybe the next month should be spent in a slower-paced town. Maybe it’s time to book a flight home for a visit. This routine gives you the permission to change your mind. It reminds you that the itinerary serves you, not the other way around.

Project and Goal Realignment for Digital Nomads

It’s easy to get distracted by the travel part of being a digital nomad and neglect the digital part. Your work provides the fuel for your journey. Every 30 days, you need to look at your professional goals.

Are you actually making progress, or are you just doing enough to get by? Use this time to clean up your digital desktop, archive finished projects, and set three major objectives for the coming month. This prevents the vacation mode creep that eventually kills many freelance careers. It keeps you sharp and professional, regardless of whether you’re working from a high-rise or a hostel.

How to Implement the Monthy Routine for Digital Nomads

The best way to make this stick is to tie it to a specific date. Many nomads choose the first Sunday of every month. Wherever you are, that day is sacred. You don’t book tours. You don’t travel to a new city. You stay put.

Start by finding a quiet space with reliable internet. Open your spreadsheets, your calendar and your journal. Be honest with yourself about what worked and what didn't. This isn’t meant to be a punishment. It’s a gift to your future self. It’s the reason you will be able to keep living this incredible life while others have to pack it in and head back to a desk.

The Long-Term Reward

The nomads who last are the ones who treat their lifestyle with respect. They know that freedom requires a foundation. By implementing a monthly reset, you’re building that foundation. You’re creating a sense of home that exists within your habits rather than a physical building.

You deserve a life that feels as good on the inside as it looks on your social media feed. That feeling starts with the boring, quiet, essential work of checking in with yourself once a month. It’s the one financial independence routine you truly cannot afford to ignore. –Abdul Rehman Jr.