Travel teaches you many things. How fragile your credit limit is abroad tends to be one of the faster lessons. Here’s what credit card management actually means when you’re traveling.

Credit card management sounds like something you do once a year with a spreadsheet and good intentions. In reality, it’s the ongoing practice of keeping your cards — credit, debit, prepaid — usable, visible and dependable when money is moving in unfamiliar systems.

At home, poor card management is inconvenient. On the road, it’s disruptive.

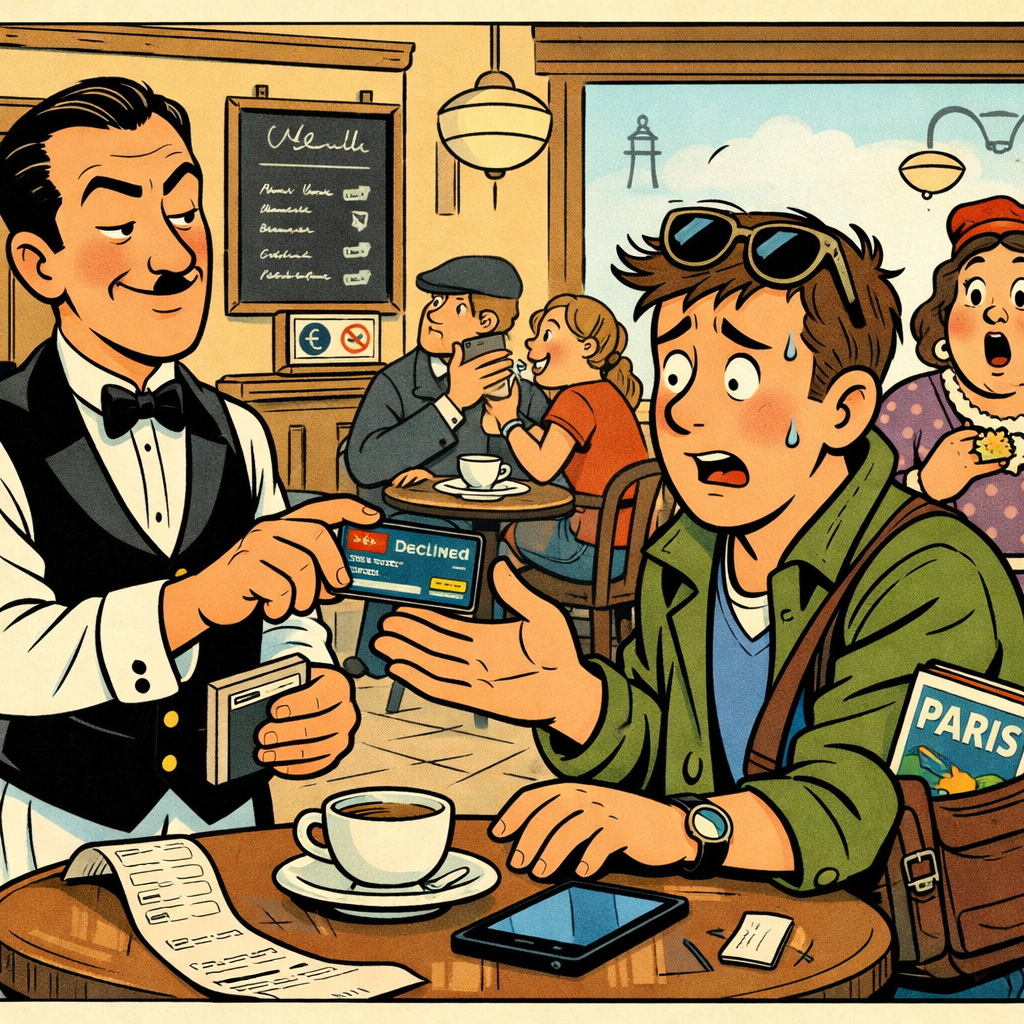

Because when your card fails abroad, it rarely fails quietly. It fails in front of a hotel desk, a rental counter, or a waiter who has already brought the check and is now waiting.

“ When your card fails abroad, it rarely fails quietly. It fails in front of a hotel desk, a rental counter, or a waiter who has already brought the check and is now waiting.”

Credit Crunch Moments Abroad

It usually starts with a hotel.

You’ve paid in advance. You’ve checked in. Everything seems fine — until you realize the property has placed a pre-authorization that quietly eats a chunk of your available credit. Then the rental car does the same. Then a restaurant charge posts as pending. Then currency conversion nudges a number just far enough to matter.

None of this is unusual. Almost none of it is explained.

Suddenly, your “plenty of room” credit limit is very much in play.

This is why card management matters more once you cross a border: International travel compresses time, money and margin for error. Charges stack faster. Holds linger longer. And the systems deciding what’s “normal” behavior are no longer familiar.

The Invisible Mechanics Draining Your Available Credit

Travelers often assume their balance tells the whole story. It doesn’t.

What affects your usable credit abroad includes:

Pre-authorizations that remain pending for days

Currency fluctuations that change final settled amounts

Merchant batching delays that make charges appear late

ATM and foreign transaction fees that post separately

Individually, these are minor. Together, they quietly reduce flexibility — especially if you’re relying on one card or traveling close to your limit.

What many people don’t realize: You can “have money” — and still be unable to use it.

When Things Go Sideways

Then there are the moments that actually raise your pulse.

A card freeze triggered by foreign spending patterns

A declined transaction for something essential

A banking app that won’t load because you’re on hotel Wi-Fi in a stone building from 1742

In these moments, card management stops being theoretical. It becomes logistical triage.

The travelers who stay calm aren’t luckier. They’re prepared.

Credit Confidence Starts Before the Airport

Good card management is front-loaded.

Before traveling internationally, experienced travelers:

Check available credit, not just balances

Review limits and upcoming payments

Notify banks of travel plans (yes, it still helps)

Pack at least one backup card on a different network

This isn’t paranoia. It’s redundancy — the same principle that makes travel adapters and offline maps a good idea.

After the Trip, the Work Isn’t Over

What happens after you return matters just as much.

Foreign charges can post days later. Holds don’t always release immediately. Fees sometimes appear after you’ve mentally closed the trip.

Strong post-travel credit card management means:

Paying balances promptly

Paying more than the minimum when possible

Reviewing statements for delayed or duplicate charges

Letting your credit recover quickly from temporary usage spikes

This is how one trip doesn’t quietly echo into your financial life for months.

The Tools That Actually Earn Space on Your Phone

This is where modern card management gets easier.

Mobile banking apps give travelers real-time visibility into balances, pending transactions and available credit — which is far more useful than checking statements after the fact.

Spending alerts, instant card freezes and secure authentication features reduce risk when something feels off.

Budgeting and currency-conversion tools add another layer of clarity, especially when you’re moving between countries with different pricing norms.

And digital wallets — Apple Pay, Google Pay — aren’t just convenient. They reduce physical card exposure and often process more smoothly abroad than plastic alone.

Why Seasoned Travelers Never Carry Just One Card

Payment infrastructure varies wildly by country. When it comes to international travel:

Some places expect chip and PIN.

Others default to contactless with low transaction caps.

Some terminals reject cards for reasons no one can explain.

Multiple cards mean:

A fallback if one is declined or frozen

Compatibility across networks and verification systems

The ability to spread spending and manage utilization

The insight here is subtle but important: Card management is about making sure you have options.

Credit Confidence on the Go

International travel will always involve financial friction — holds, fees, delays and the occasional decline. The difference between stress and confidence is understanding how those systems behave and planning accordingly.

When travelers manage cards proactively, use tools that provide real-time awareness, and build in redundancy, money becomes a background system instead of a recurring problem.

And if that still feels like too much to navigate alone, a trusted financial professional can help create a strategy that supports both travel habits and long-term credit health.

Because the best travel memories come from what you saw, ate and wandered into — not from the moment your card didn’t work and everyone was watching. –Mashum Mollah

Mashum Mollah is the founder and CEO of Blog Management. He also runs the site Blogstellar.